11 questions about the coronavirus economic crisis you were too embarrassed to ask

From how to think about the stock market to what to do if you lose your job, here’s what you need to know about coronavirus and the economy.

By

Emily Stewart

Apr 2, 2020, 8:00am EDT

Share this story

-

Share this on Facebook

-

Share this on Twitter

-

Share

All sharing options

Share

All sharing options for:

11 questions about the coronavirus economic crisis you were too embarrassed to ask

-

Reddit

-

Pocket

-

Flipboard

-

Email

This story is part of a group of stories called

Evidence-based explanations of the coronavirus crisis, from how it started to how it might end to how to protect yourself and others.

The American economy seems to have transformed in a matter of weeks as the coronavirus has brought activities across the country to a grinding halt. Not only did the US fail to anticipate the public health crisis caused by coronavirus, but it appears to be unprepared for the economic consequences of getting the pandemic under control.

Most Americans already know they are in a very different economic reality than they were in February. Restaurants are closed or only doing takeout or delivery. Clothing boutiques are shuttering. Americans across the economy have lost their jobs. Even workers whose jobs might be more stable probably don’t want to look at their 401(k)s.

Government officials have made a conscious decision to lock down parts of the economy and implement strict social distancing guidelines to try to better respond to the pandemic. President Donald Trump initially said he’d like to reopen the economy by Easter to avoid further damage — perhaps thinking it’s better to just keep the economy going and let the chips fall where they may — but people aren’t going to be falling over themselves to go to restaurants if there’s a deadly virus spreading. Trump ultimately backed off, and extended social distancing measures to the end of April. After all, the point of the economy is to serve people, not for people to serve it.

Related

The missing piece in the coronavirus stimulus bill: Relief for immigrants

“There seems to be a segment of society that’s lost track of the purpose of markets,” said Aaron Klein, the policy director at the Center on Regulation and Markets at the Brookings Institution. “Humanity created markets to efficiently distribute goods and services to serve humanity; markets did not create humanity to efficiently serve the will of the markets.”

We’re stuck in dual crises for the foreseeable future — one that’s health-related, and one that’s economic. Eventually this will end, but there’s no telling when. It’s a confusing time, including when it comes to the money-related end of things. So here are some answers to questions about the economic crisis that you were perhaps too embarrassed — or too afraid — to ask.

1) What is an economic crisis?

An economic crisis is a steep and sudden downturn of the economy. In terms of data, it shows up in a lot of places — GDP growth, unemployment numbers, productivity, and more. Data often lags behind real-time events, but what we already know paints a dire picture: an enormous spike in jobless claims and an economic contraction projection of disturbing proportions.

The US is definitely in an economic crisis right now, albeit a distinct one from crises past, including the one in most recent memory: the financial crisis and Great Recession in the late 2000s. “The prior recession started in the financial markets and affected the real economy; this will start in the real economy and affect the financial markets,” said Klein.

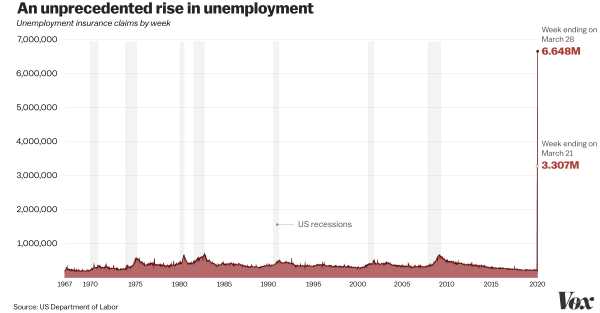

The problem right now isn’t subprime mortgages and banks and hedge funds making bets they shouldn’t — it’s that the US in the midst of a global health crisis and is taking extreme economic measures in an effort to protect the public’s well-being. Public officials have ordered shut wide swaths of the economy, including restaurants, travel, and hospitality, and it’s had a severe and immediate effect. Jobless claims hit 6.6 million during the last week of March, double the unprecedented 3.3 million claims from the week prior. During the Great Recession, the highest week of losses was about 600,000, and 8.7 million total jobs were lost over the course of many months. Factories across the country have shut down, businesses are shuttered, and not only do people have less money to spend, but they have fewer ways to spend it.

“Everything this time is happening bigger and faster,” Jason Furman, who served as an economic adviser to President Barack Obama, told Vox’s Li Zhou and Ella Nilsen recently in a piece laying out the differences between the 2008 crash and now.

The question now is if and when the US is able to get the virus under control so that the economy can start to open back up. “What we need is for everybody to stay home and not go broke doing it,” said Cecilia Rouse, an economist at Princeton and former member of Obama’s Council of Economic Advisers. “The faster we can get this pandemic under control, the faster we can snap back.”

The longer the crisis goes on, the more challenging the recovery becomes, and the longer it will take.

2) What’s the difference between a recession and a depression?

There’s a well-known line among economists that a recession is when your neighbor loses their job, but a depression is when you lose yours, which perhaps gets at the air of difference between the two: A recession feels bad, a depression feels very bad. But the line between recession and depression can be a little fuzzy.

Traditionally, a recession is defined as two consecutive quarters of negative GDP growth, but the National Bureau of Economic Research (NBER) has a broader definition of a “significant decline in economic activity spread across the economy” that lasts for more than a few months and shows up in places like GDP, income, employment, production, and retail sales. In the US, a group within the NBER is officially charged with “calling” when a recession starts and ends — and it usually takes them some time after a recession begins for them to say it’s happening.

A depression, on the other hand, is a more severe and prolonged version of a recession. The Great Depression that lasted from 1929 to the early 1940s included not one but two major economic downturns — one from 1929 to 1933, and another from 1937 to 1938. Output fell sharply.

The coronavirus recession could indeed become a depression. The US is in uncharted territory in what’s going on in the economy — Americans have stopped working, stopped producing, and stopped consuming almost at the drop of a hat. The stock market is volatile, and business investment is slowing. Much of the country has been ground to a halt.

Whether or not the US slips into a depression depends in large part how well Americans are able to weather the storm while the coronavirus portion of the crisis gets figured out. Officials don’t want the economy to become so broken that it can’t be fixed.

“Ultimately, the economy will rebound when the pandemic is under control. The question is, how many businesses will be able to weather the storm, and how many workers will be able to?” Klein said. “The longer the shutdown goes on, the greater effects on the economy, particularly if businesses can’t reopen.”

It’s also important to note that, whatever you call it, not everyone will experience the economic fallout in the same ways. For some people, it will be catastrophic. For others, it will be an inconvenience. Older, low-income, and homeless people and those in other vulnerable communities will also likely experience the economic crisis in more harmful ways, regardless of how the downturn is defined formally.

3) What does the stock market have to do with any of this?

The stock market has been all over the place amid the coronavirus crisis. Major indexes plunged as the gravity of the situation began to take hold in February and March, and stocks have become pretty volatile. But does it matter what the stock market does? Well, yes and no.

The stock market right now is signifying underlying turmoil in the economy. It can also be a leading indicator, albeit a noisy one, of where the economy might be headed, and amid coronavirus, its take appears to be ¯_(ツ)_/¯. As stocks plunged at the takeoff of the crisis in the US, a lot of investors appear to have pulled out their money and parked it in cash, and uncertainty has created an enormous amount of volatility.

The stock market will likely start to recover before the economy does — that’s what happened after the financial crisis, when it turned up in March 2009 and the recession ended three months later in June — but we won’t know if or when that will be. What happens in the stock market can have a “wealth effect” as well that is largely behavioral — consumers spend more in a bull market. A small majority of Americans own stocks, but the richest Americans own most of the stocks.

But the average person shouldn’t focus too much on what’s going on in the markets, especially in the short term. There’s a saying from legendary investor Benjamin Graham that the market is a voting machine in the short run but a weighing machine in the long run. A stock’s particular price might be up or down on a given day, but ultimately, the underlying fundamentals of a business are what matters.

“What we know about anything that is bought and sold is that price is dictated by price and demand. What helps determine stock prices over the long run, of course, is earnings, it’s fundamentals, but in the short run, panic can create very significant mispricing,” said Kristina Hooper, chief global market strategist at Invesco.

There have also been questions about whether the US could halt stock market trading altogether, beyond the temporary “circuit breaker” stops that are triggered when stocks drop too much. Greg Daco, an economist at Oxford Economics, told me that theoretically it could — after all, there are stock market holidays — but that wouldn’t necessarily solve the volatility problem. “The question is, what happens when it reopens?” he said. “You close the market, reopen it, and it falls by 30 percent, was it worth it?”

4) If I have investments, like a 401(k), what should I be doing?

The best advice right now on what to do on your investments, per finance experts, might also be the hardest to follow: Do nothing.

“Most people are horrible at making long-term investment decisions generally, and that’s exacerbated when they try to make decisions under emotionally intense circumstances,” said Zach Teutsch, a financial adviser at Values Added Financial.

While it may be tempting to look at your 401(k) or stock portfolio right now, it might not paint a pretty picture and could prompt you to make decisions you might later regret. That’s part of what happened in 2008, Hooper said, when average Americans paid too much attention to the stock market, pulled their money out, and then missed out when stocks started to come back. “One of the biggest mistakes in the financial crisis was that the average American did focus on it, and many of them changed their asset allocations as a result,” she said.

Remember, before the current crisis, Americans were in the midst of the longest economic expansion in US history and a multi-year bull market.

To be sure, the advice around this changes with age — people who have years before they plan to retire can wait out the recovery, while those close to or in retirement might not be able to. The experts I spoke with said older people have hopefully shifted their investments toward less risky places — more bonds than stocks, for example — with age. (There’s a reason your 401(k) investment plan often has a target retirement date attached to it.)

For younger people, or those with some money to spare, down markets can be a good time to get in. If you can afford to kick up your 401(k) contributions, consider it. Or if you have cash on hand, a lot of stocks might be trading at a discount. “If you needed to buy a new pair of shoes and all the shoes in the world were 40 percent off, you wouldn’t say, oh, no, there’s a terrible shoe crisis, you’d say, terrific, I can get the shoes I need for cheaper?” Teutsch said.

“Young people make a fortune on stock market crashes, because they’re adding every couple of weeks in bad markets at lower prices; you just don’t get to see it or appreciate it until years down the line,” said David Bahnsen, a portfolio manager and financial commentator.

It’s important to remember investing has inherent risks, there are no guarantees, things could get much worse before they get better, and the market is next to impossible to time — Warren Buffett once bet the S&P 500 would outperform a basket of hedge funds for a decade. And he won.

5) How does unemployment insurance work?

The first thing to know about unemployment insurance is that it’s a state-federal program that provides cash benefits, but in terms of administration, it goes through the state. In other words, it’s pretty patchy. So to apply, you need to go through your state unemployment agency, and guidelines for who qualifies and what benefits are awarded vary. You can find information about your state’s requirements and processes here.

First, we’ll go through the typical scenario for unemployment insurance, and then through the changes in the pandemic and how the stimulus package fortifies the program.

If you have been laid off or fired by an employer and have a “substantial history” of working, then you can apply to collect unemployment insurance benefits on a weekly basis.

Once you start the application process online or by phone, the unemployment insurance office contacts your employer to confirm that your explanation of why the job ended matches up. If the explanations for the separation are in agreement, then the claim generally moves forward quite quickly. If not, then there’s a dispute, and the state makes a judgment of what happened. It is worth noting that people who quit their jobs can also file for unemployment — for example, in cases of sexual harassment — but those workers are likelier to lose in the dispute.

Related

Coronavirus could lead to the highest unemployment levels since the Great Depression

“When there are disputes over what happened, if people are laid off, they collect benefits 70 percent of the time. If there’s a dispute and they quit, they get benefits about 25 percent of the time,” said Wayne Vroman, a labor economist at the Urban Institute.

The amount you’re eligible to receive is calculated based on what you were earning at your job, and maximum and minimum amounts vary by state. Many states allow you to collect benefits for a maximum of 26 weeks, but again, that varies. Vroman estimates that the average across the system is about $385 a week. Across 52 weeks, that would add up to about $20,000 under the pre-stimulus system — in other words, it’s not a replacement for a full-time job, plus you can’t use it for a full year anyway. Typically, there are limits on how much you can earn while you’re collecting benefits. In other words, no side gigs or freelancing.

Unemployment insurance is funded through payroll taxes paid by employers, and when there are a lot of claims, states can run out of money to pay benefits out. During the last recession, three dozen states wound up having to borrow from the federal government to cover unemployment insurance.

Because so many people are filing for unemployment amid coronavirus, doing so is extra challenging right now, and many state offices are overwhelmed. That may translate to delays for those filing.

The late March stimulus package puts unemployment insurance on steroids. It includes a $600 per week increase in unemployment benefits on top of state benefits for four months. It also expands unemployment to people who aren’t usually covered — gig workers, freelancers, contractors, the self-employed, and workers who are furloughed or have reduced hours — and allows for 13 weeks to be tacked on to each state’s maximum.

“If you lose your job, if your hours are cut, and even if it doesn’t feel like you’ve lost your job but you’ve been put on a zero-hour schedule, you can still apply for unemployment benefits even if your employer tells you you can’t,” said Andrew Stettner, a senior fellow at the Century Foundation.

Vox’s Dylan Matthews has an explainer on how the stimulus bill changes unemployment insurance.

6) How do I pay for health care if I’m laid off?

In the United States, health coverage is tied to employment. Now, large parts of the economy have been shut down in order to respond to a health crisis, resulting in millions of Americans losing their jobs in the middle of said health crisis and, therefore, many of them losing their health insurance.

“The joy of picking — or keeping — your health insurance is really predicated on you having a job,” said Mike Konczal, a fellow at the Roosevelt Institute.

Linda Blumberg, a health system expert at the Urban Institute, talked Vox through what to do if you are laid off and lose your employer-based insurance.

The first step for people who can afford it is to look into the potential for getting COBRA coverage, which basically means you get to hold on to your insurance but pay for it yourself. But COBRA can be expensive and translate to thousands of dollars in premiums. For people whose incomes have fallen significantly, and especially for those who live in Medicaid expansion states, Medicaid is another place to look. You can see if you qualify for Medicaid in your state based on your income here. For children, you can look into CHIP as well.

People who lose their jobs can also enroll in the Affordable Care Act marketplaces for a certain period, because losing your health insurance, as well as having a baby or getting married, is considered a “qualifying event.” And there, you may be eligible for subsidies, too. Blumberg cautioned people should be thorough in looking for options for enrollment, and they should presume their loss of income is going to persist when inputting information into the system. “If for some reason they get their job back or their hours come back up, they can then report that at the time and have the subsidy reduced,” she said.

Even if you’re not eligible for a subsidy, it’s an especially critical time to have health insurance, given the coronavirus outbreak.

Blumberg warned against nongovernment, non-marketplace plans and “short-term, limited-duration” plans allowed under the Trump administration. “Those other policies, it’s very difficult, often, to figure out what’s excluded from them,” she said. “Be very cautious of something that looks too good to be true.”

For those who are uninsured already, it’s worth noting that some states have reopened their marketplaces in light of the crisis, so you may be able to get insurance now. “Debt is better than dead,” Blumberg said.

Vox’s Dylan Scott has an explainer on health insurance amid coronavirus and the different mechanisms for coverage. He also notes that the CDC said in a statement to Vox that the agency believes it has the legal authority to cover Covid-19 testing and treatment, in collaboration with other federal and local agencies. In a separate statement, a CDC spokesperson told Vox that there are “provisions that allocate funding for testing and treatment of the uninsured, which will continue to be announced” and noted that federally qualified health centers are an important resource for those who lack insurance.

7) What other mechanisms are there to help me if I can’t pay my bills?

Beyond unemployment and health insurance, there are other ways out there to help people make ends meet.

For example, there are multiple options for food assistance, including SNAP benefits (more commonly known as food stamps) and specific services for pregnant or postpartum women and children and seniors. In the case of food stamps, they’re managed by the states, and you can find a directory here. Food stamps, like other assistance programs, are pegged to your income.

“It’s possible that you have, even with unemployment insurance, an income that’s low enough that you would be eligible for SNAP,” Vroman said.

You can also find an outline of government benefits here.

Stettner advised that people should start signing up for benefits and assistance programs as soon as they can. “Start the process, because it can take some time. Don’t wait around to the last minute to reach out for help,” he said. He added it’s also worth reaching out to utility companies in the case of hardships to see if they’ll work with you on a plan to pay your bills. (The same may apply for rent payments or mortgages, too.)

Unfortunately, a lot of the safety net in the US has been whittled down over the years. “It’s for the most needy people in our society, so we don’t have a lot of room for people just getting by,” Rouse said.

8) How does the stimulus work, and what else is the government doing to help the economy?

On March 27, the president signed a $2.2 trillion stimulus package, the CARES Act, to help stabilize and boost the American economy in the time of coronavirus. Vox’s Li Zhou and Ella Nilsen have a full explainer of what’s in the bill, and here’s a brief overview:

- A $500 billion loan program for businesses to be administered by the Treasury Department. Basically, a bailout fund for big business.

- Boosted unemployment insurance that increases benefits by $600 a week per four months and expands who can apply for and collect benefits

- Funds for hospitals, medical equipment, and protection for health care workers totaling $150 billion, $1 billion of which will go to hospitals, $1 billion to the Indiana Health Service, and the rest to increased medical equipment capacity

- Roughly $150 in aid to state and local governments, including $5 billion for tribal governments

- About $377 billion in small business loans

The other plank of the stimulus, which has gotten perhaps the most attention is the direct payments to be sent to Americans across the country — in other words, those checks from the government you’ve probably been hearing about. (Vox’s Dylan Matthews has an explainer on the stimulus checks.)

Single adults who make up to $75,000 annually will get a one-time $1,200 check, and married couples who make up to $150,000 will receive $2,400. The government will also distribute $500 per child. The payments decrease as incomes go up and phase out by $99,000 for singles and $198,000 for couples. The calculations will be made using 2019 taxes for those who have filed (the deadline is now July 15) and 2018 taxes for those who have not. There are several calculators online you can use to figure out how much you’ll receive.

For those who don’t file taxes because they earned so little they weren’t required to, collecting the cash will be more complex. The IRS says people will need to file a “simple tax return” with basic information to collect money, and low-income taxpayers, older people, Social Security recipients, some veterans, and individuals who otherwise don’t need to file a tax return will not owe tax. Note that people in households with members who are unauthorized immigrants may be ineligible for the direct payments.

Beyond the stimulus bill, Congress has passed two other coronavirus-related pieces of legislation, and the Federal Reserve has taken steps to help stabilize markets and the economy. Democrats are pushing for a fourth coronavirus bill, but thus far, it’s not clear how much buy-in there is from Republicans.

As for what else the government could be doing, the answer is plenty, if there’s political will. Americans are facing a health and economic crisis of staggering proportions, and the greater risk is doing too little than in doing too much. Vox’s Matt Yglesias recently laid out some possibilities:

“Does anybody regret how much debt we went into to win World War II?” said Betsey Stevenson, an economist at the University of Michigan and former Obama administration official. “People rarely complain about how much Congress is spending to fight a war, and they need to be thinking about that right now as we fight this pandemic.”

9) Which industries are being hit hardest by this?

Not every person — or every sector — is being impacted equally by the coronavirus crisis.

“This recession is going to be, for some people, more devastating than the financial crisis, for some less,” Klein said. “This one is going to start further down on the income spectrum.”

Restaurants, bars, stores, and nonessential businesses have been forced to close across much of the country. Airlines have seen an enormous decline in business, as has the travel and hospitality industry across the board. Schools have been shut down and live entertainment brought to a stop.

The stimulus bill is meant to bring some relief to both small businesses and major corporations, which both got bailout funds as part of the $2.2 trillion package. But, again, it really depends how long this lasts to see how hard the economy to be hit.

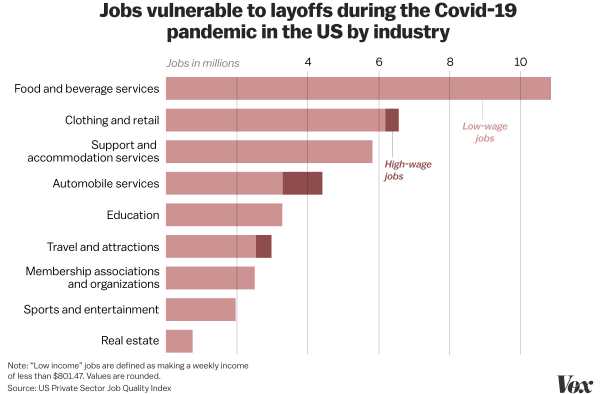

Ultimately, businesses and industries translate to people, as in, workers, and the workers who will be hardest hit by layoffs and shutdowns are those who can’t afford it. According to estimates from the US Private Sector Job Quality Index, more than 37 million jobs in the US are vulnerable to layoffs in the near term, 35 million of which are considered low-income.

There will likely also be disparities by race and ethnicity.

“We know that blacks, Latinx, and native people, in terms of race and ethnicity, they have lower levels of reserves, and we also know that their employment is more precarious than that of white people,” said Darrick Hamilton, the executive director of the Kirwan Institute for the Study of Race and Ethnicity at Ohio State University.

10) How can I spend money to help?

If you have extra cash on hand right now and aren’t concerned about parting ways with it, there are plenty of things to do with it to try to help — order delivery from local restaurants and grocery stores, or buy gift certificates for local businesses that you can use at a later date. Amazon is one company not worried about its business right now, so maybe get toilet paper from the market down the street instead. Tip the delivery person generously. Instead of ordering through a delivery app, try calling the restaurant instead. Lower-wage service workers are going to be the ones hurt the most the fastest.

“A lot of small businesses that tend to work on fairly small margins to begin with are going to be very hard hit,” Rouse said.

If you employ people, such as a child care provider or cleaning service, you can always keep paying them, even if you ask them not to come.

There are plenty of charities willing to take your money, including GiveDirectly, which is providing cash assistance to families. You can also contact local food banks and other social service organizations to figure out how you can help. Another grim reality is that there are plenty of GoFundMe accounts set up to provide economic and medical aid.

But the fact of the matter is, there is only so much that private individuals can do.

“Fundamentally, this needs to be a government solution. Individual acts of charity or trying to keep the economy afloat are not sufficient at this moment,” Konczal said. “The recession is ultimately a collective problem, and the government will be the one who determines what happens to small business, self-employed people, and so on down the line.”

11) When will things get better? Is there a chance any of this brings about positive change to the economy?

At the moment, the likeliest scenario is that the economy gets better when the coronavirus crisis gets better, and unfortunately, nobody knows when that will be. As Dartmouth College economist Bruce Sacerdote put it, “It’s all about getting the damn virus under control.”

There has been some debate about whether the “cure” — as in the economic shutdown — is worse than the disease that is coronavirus. And some people have suggested government officials open the economy back up and start to ease restrictions on social distancing even before the health plank of this is under control. But is it really worth sacrificing tens of thousands of people so that the Dow Jones Industrial Average will go back up? And is it really likely that with a deadly virus spreading, people are going to be eager to go eat at the diner down the street?

Billionaire Bill Gates recently weighed in: “It’s very tough to say to people, ‘Hey, keep going to restaurants, go buy new houses, ignore that pile of bodies over in the corner. We want you to keep spending because there’s maybe a politician who thinks GDP growth is all that counts.’”

Vox’s Ezra Klein also recently did a deep dive:

So for now Americans are in a waiting game with the virus, and once that’s under control, the recovery will depend on the mitigation measures the US has taken and will take. “The debate is if we end up in a V-shape or a U-shape recovery, and anyone who pretends to have the answer to that is wrong,” Bahnsen said.

As to whether this will bring about positive change in the economy, it’s hard to tell. On the one hand, policies and government actions that would have seemed almost unimaginable just weeks or months ago — a check going out to nearly every American household, expanding unemployment insurance — are now a reality. And in such a scenario where so many Americans are losing health coverage in the time they need it most, it has to make some at least think about the value of Medicare-for-all, or at the very least, a public health insurance option. The Great Depression resulted in a dramatic expansion of the social safety net.

“We’re considering this use of public power to address our calamity in ways that the public imagination didn’t consider in the past. The sobering reality is that it’s not enough,” Hamilton said. “You can’t tell people that this stuff is impossible, because it happened.”

This could also foster a discussion about how Americans treat and think about the workers deemed “essential” during times of crisis, which includes not only doctors and nurses but also home health care workers, grocery store clerks, and service staff.

On the other hand, there’s always a tendency to revert to the mean, and recessions and economic crises don’t usually make Americans more generous. “In general, recessions make people very zero-sum and very hesitant to want to collectively provide security. We saw that in the Great Recession,” Konczal said. “We should not understand this as an obviously political moment.”

Sourse: vox.com