Public understanding of clean energy has not kept up with reality. The popular perception is still that clean energy is virtuous but expensive and unreliable, that it needs special favors to compete in the marketplace.

In fact, in a growing number of places, the inverse is true. Clean energy has become cheaper than the dirty stuff, but it has trouble competing because markets are rigged on behalf of fossil fuels. More open, competitive markets would benefit clean energy.

For a convincing illustration, look no further than the states in the American South (Alabama, Florida, Georgia, Mississippi, North Carolina, South Carolina, and Tennessee).

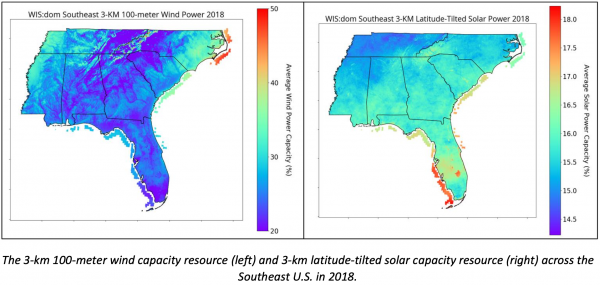

While clean electricity has begun transforming markets in almost every area of the US, it has largely bypassed the South, which has the lowest installed solar and wind capacity of any US region, despite fairly abundant renewable energy resources.

That’s not because fossil fuel electricity is winning in the market. It’s because there are no markets. The entire system is run by monopoly utilities with little incentive to innovate.

The research firm Energy Innovation recently took a close look at what would happen if the South’s electricity system was opened up to greater market competition — if the cheapest options could be selected and shared across the region.

The effect would be dramatic: By 2040, vastly more renewable energy and batteries would be deployed, average retail electricity prices would be down by 23 percent, cumulative savings for the region’s ratepayers would reach approximately $384 billion, greenhouse gas emissions would fall by 37 percent from 2018 levels, air pollution would plunge effectively to zero, and 385,000 additional jobs would be created. It’s a win-win-win-win-win-win situation.

And keep in mind: this is only through market competition, without assuming any additional policies to support clean energy. Given the current cost environment, competitive energy markets, left to their own devices, rapidly decarbonize.

We’ll look at the details in a moment. First, a little background.

The South’s electricity system is run by energy monopolies

In the beginning, there were monopoly utilities. Around the turn of the 20th century, they were established with the goal of electrifying America. The deal, their “social contract,” was as follows: In a given region, a single entity would be given monopoly control over electricity, from generation to delivery (it would be “fully integrated”). It would not make money from the sale of electricity — it would not be fair for a monopoly to set its own prices. Rather, it would sell electricity at cost. Its profits, its incentives, would come from the building of electricity infrastructure, the power plants and power lines needed to extend electricity to everyone in the country. Utilities receive a guaranteed rate of return (around 8 percent) on those investments.

In exchange for these guaranteed profits, utilities agreed to provide universal access to reliable, low-cost power and to answer to state regulators, who would set their power rates and determine their returns. These regulators are known as public utility commissions, or PUCs.

This worked well for a while, but toward the end of the 20th century, it became clear that it isn’t efficient for each utility to build its own power plants and maintain its own reliability reserves. It led to massive overbuilding and unnecessarily high prices. So in the 1980s and ’90s, a wave of “restructuring” washed over the industry.

In restructured markets, energy generation (building and operating power plants) was separated from power delivery through local distribution grids. Generation companies (gencos) built and operated power plants and sold their power in competitive, cross-utility regional markets; distribution companies (discos) bought power from those markets and delivered it to customers. Regional markets and long-distance, inter-state energy transmission are overseen by Regional Transmission Organizations (RTOs) or Independent Service Operators (ISOs). (They are, for all intents and purposes, the same thing.)

ISOs and RTOs now serve about 70 percent of power customers across the nation. And though energy wholesale markets have been, and are, the subject of much dispute, it is generally agreed that competition has served ratepayers well.

Related

Power utilities are built for the 20th century. That’s why they’re flailing in the 21st.

But not in the South. The South remains entirely dominated by old-school, unrestructured, fully integrated utility monopolies like Florida Power & Light and Duke Energy. Each utility operates its own fiefdom, builds its own power plants and transmission, maintains its own reserve margins, and enjoys a cozy relationship with its PUCs.

This setup has several consequences. First, because these utilities make their profits based on how much they invest in power plants and power lines, they want to build (and maintain) power plants and power lines. They have no incentive to share across territories, or to economize.

Second, each fiefdom must maintain its own reserve margins, so there is a built-in excuse for overbuilding. Third, there is no competitive power procurement or deployment process. Utility executives decide what to build and then convince regulators, so there is little restraint on overspending.

Finally, once a fully integrated utility builds a power plant, it has every incentive to keep that plant running — even if it’s losing money, even if there are cheaper alternatives — because it gets paid a guaranteed rate of return on the investment.

All of this adds up to a lousy way to run a railroad: utilities with every incentive to overspend, overbuild, overcharge consumers, and fight off competitors.

How much better could they do with a little competition? That is what Energy Innovation — with the help of the energy modelers at Vibrant Clean Energy — set out to determine. Their results are here, including a modeling report, a policy report, and a data visualization dashboard.

The short answer is that the South could lower emissions, improve public health, and reduce the cost of power by establishing a competitive region-wide energy market.

Competition would reduce power costs in the South

There are different levels of reform the South’s regulators and utilities could undertake.

The milder reform, called an energy imbalance market (EIM), is currently being discussed by Duke, Southern Company, and a few other southern utilities.

In the West — the only other region of the country not covered by RTOs and ISOs — they have what’s called the Western Energy Imbalance Market, which allows some trading of energy among utilities on an hour-by-hour basis. Southern utilities are discussing a similar “centralized, region-wide, automated intra-hour energy exchange” called the Southeast Energy Exchange Market (SEEM).

The Energy Innovation report warns that SEEM “is likely even less transformative than the more incremental [Western] EIM, as SEEM details to date do not indicate EIM benefits such as an independent operator, transparent pricing, or transmission access rules.” They call the approach “an unambitious and incremental approach to increasing competition.” It would help — more on that in a moment — but it falls far short of what a full regional market could do.

And then there’s the more ambitious option, a competitive regional energy market administered by an RTO, with enough transmission to share energy and reserves across territories.

Vibrant Clean Energy modeled the RTO scenario using “the first commercial co-optimization model of energy grids that was built from the ground up to incorporate vast volumes of data, starting with high-resolution weather and demand data.” The model automatically seeks the lowest-cost resources that will maintain reliability.

Vibrant compared a business-as-usual scenario, based on the Integrated Resource Plans (IRPs) of the utilities themselves (assuming no additional policy), to a scenario with full market competition.

The results are dramatic, most notably in that market competition would wipe coal out in short order, along with most natural gas.

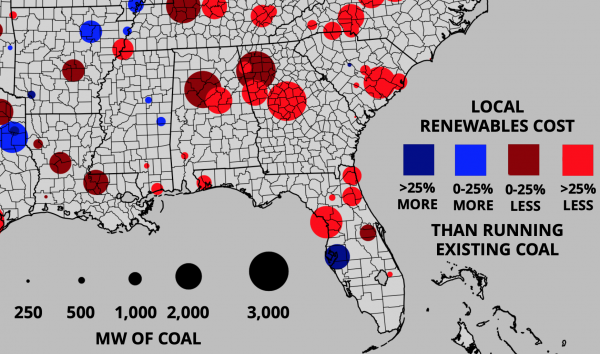

In 2019, Energy Innovation and Vibrant partnered to compare the cost of running the nation’s existing coal plants to the cost of building new, local wind and solar power plants. The report found that about two-thirds of US coal plants are more expensive to run than new renewables are to build and run. But for the Southeast, the results were even more striking: 92 percent of the region’s existing coal plants are more expensive to run than new renewables are to build and operate.

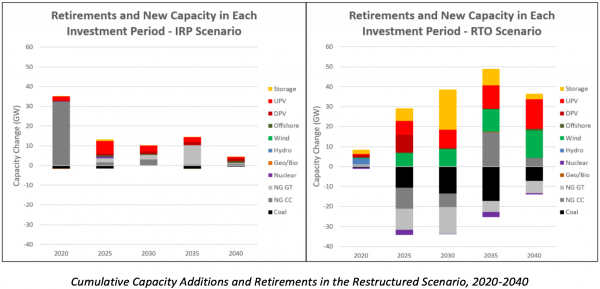

In the IRP scenario, the South’s uneconomic power plants mostly stay in place and more gas plants are added. When the region’s power system is opened up to competition, it prompts a wave of fossil fuel plant retirements and new renewable energy capacity.

“In the IRP Scenario, there is almost no wind generation and solar PV provides just 4 percent of annual generation,” the report finds. “In contrast, wind and solar provide 22 percent of generation in the RTO Scenario; when aggregated with nuclear (20 percent), geothermal/bioenergy (5 percent) and hydropower (4 percent), 51 percent of the Southeast fleet is zero-carbon by 2040 in the RTO Scenario.”

Overall, the RTO scenario produces 131 gigawatts of new renewables and storage (52 GW of solar, 42 GW of wind, 37 GW of storage), compared to 21 GW under the IRP scenario. It would also retire all coal plants and most natural gas peaker plants by 2040.

The substitution of cheaper renewables for uneconomic coal and natural gas plants would bring a whole range of benefits.

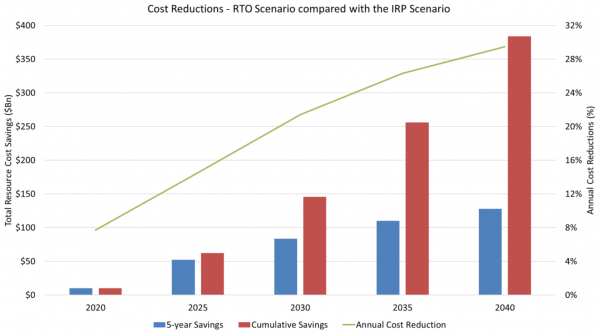

First, it would immediately start saving ratepayers money. In 2025, the first year the RTO is fully set up and running, it would already be $13 billion cheaper to operate. And by 2040, the cumulative savings add up to $384 billion, with rates eventually falling 29 percent lower than in the IRP scenario.

These savings are accomplished through “improvements on the inefficiencies of a balkanized, uncompetitive approach to transmission planning, resource adequacy, integration of distributed energy resources, and dispatch throughout the region,” the report says. It is simply cheaper and more efficient for utilities to cooperate.

(Worth noting: Around $38 billion of these savings, or 10 percent, come from optimizing distributed resources — rooftop solar panels, batteries, etc. — to which southern utilities have traditionally been quite hostile.)

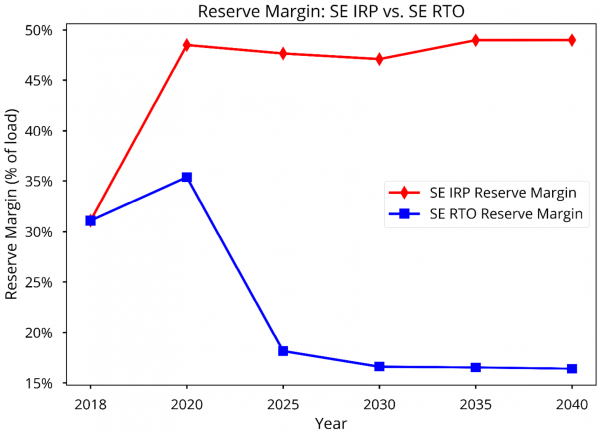

Recall that each utility has to maintain its own reserve margin — spare generation capacity that can be brought online in case of unexpected surges in demand or the loss of a power plant. If all the reserves of all the utilities across the South are added up, the “combined planning reserve margin (PRM) of the region reaches 48 percent in 2040,” the report says. That means there will be enough power capacity to meet a simultaneous demand peak across the entire region — plus 48 percent.

It’s ludicrous. The North American Electric Reliability Corporation, which develops and enforces reliability standards for the North American grid, sets a reference PRM target of 15 percent. Cumulatively, the South is heading for a situation in which it has more than three times the reserve power capacity it needs. Monopoly utilities are profiting off all those pointless extra power plants, but they are costing ratepayers money.

The RTO scenario would bring the region-wide PRM down to a more reasonable 16 percent.

Market competition would also reduce pollution and create jobs

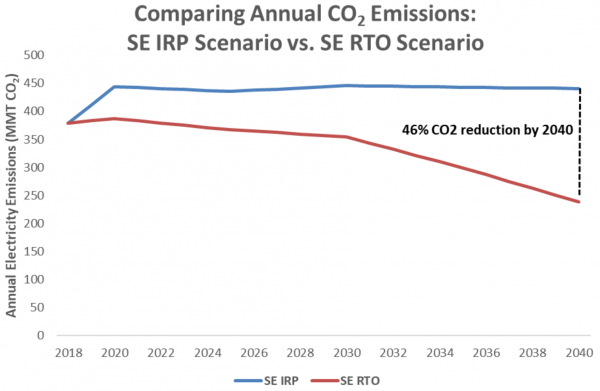

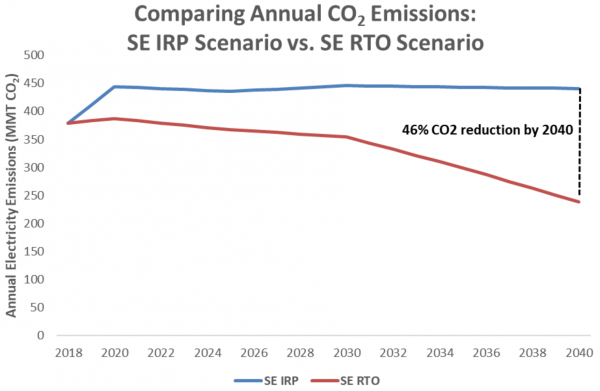

Because market competition would draw in a flood of zero-carbon renewables, the RTO scenario would also accelerate carbon reductions. Specifically, it would reduce greenhouse gas emissions 46 percent relative to the IRP scenario (in which emissions actually rise). By 2040, emissions would be 37 percent lower than 2018 levels.

In addition, emission of common air pollutants like soot and sulfur dioxide would fall to near zero by 2040. As recent research has shown, air pollution is doing much more damage to human welfare than has been appreciated. When the public health and economic benefits of reduced air pollution are added to the financial savings, the case for a rapid clean energy transition becomes unassailable.

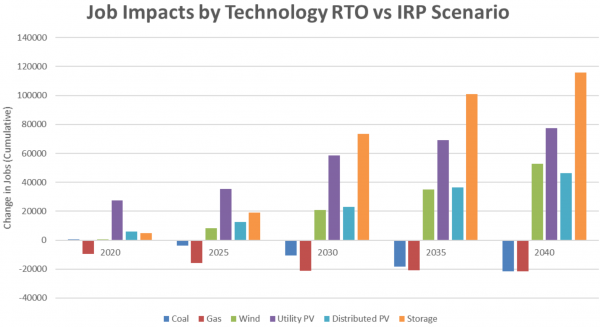

Finally, competitive energy markets would also bring many more jobs to the South. “Overall, by 2040, the RTO Scenario leads to an additional 408,000 jobs in the sector,” the report finds, “compared to just 122,000 new jobs in the IRP Scenario.” That’s a net advantage of 285,000 jobs for clean energy.

Most of these jobs would come in building out wind, solar, and batteries. Jobs maintaining old, unnecessary fossil fuel power plants would be lost, but nowhere near as many as would be created.

The report doesn’t consider manufacturing jobs that might be attracted to the region, or the economy-wide stimulus that might be provided by cheaper electricity, so these job estimates are almost certainly conservative.

Even competitive procurement within utilities would save Southerners money

Vibrant also ran a couple of side scenarios that are worth highlighting.

One models the RTO scenario, but with all the region’s nuclear power plants kept open rather than retired. It results in total system costs just a smidge (0.5 percent) higher than the straight RTO scenario, but because it avoids lots of natural gas capacity, it has substantial air quality benefits.

In the other scenario, called “economic IRP,” there’s no regional market or RTO or trading among utilities; each utility territory remains a self-contained island. However, power procurement and dispatch are done based on a cost-optimization model rather than the utilities’ IRPs.

Remarkably, by 2040, this change alone produces about three-quarters of the cumulative savings ($298 billion) produced by the RTO scenario.

“Simply optimizing for cost generates orders of magnitude greater deployment of wind, solar, and batteries, plus rapid coal phase out,” says Energy Innovation’s Mike O’Boyle. “Utilities and their planning regimes, rather than economics, seem to be the main barrier to regional renewables deployment.”

Fully integrated monopoly utilities are not truly set up to provide consumers with least-cost power, despite their social contract. They are slow to change, much too slow to keep up with the precipitous decline in renewables costs. They make money by keeping fossil fuel plants open; consumers save money when fossil fuel plants close. “Nothing in monopoly regulation encourages the adoption of new technology or risk taking,” O’Boyle says.

Southern utilities should establish an EIM if that’s the best they can do — it’s better than nothing. But Southerners should push for more. They should strive to break the grip of hidebound monopoly utilities and create a fully regionalized market that reduces power prices, air pollution, and greenhouse gases.

And advocates should carry the message to the public: Clean energy is cheaper than the dirty stuff, and the freer and more competitive markets become, the more clean energy they will produce. Every American, including those in the South, deserves to share in the benefits.

Help keep Vox free for all

Millions turn to Vox each month to understand what’s happening in the news, from the coronavirus crisis to a racial reckoning to what is, quite possibly, the most consequential presidential election of our lifetimes. Our mission has never been more vital than it is in this moment: to empower you through understanding. But our distinctive brand of explanatory journalism takes resources — particularly during a pandemic and an economic downturn. Even when the economy and the news advertising market recovers, your support will be a critical part of sustaining our resource-intensive work, and helping everyone make sense of an increasingly chaotic world. Contribute today from as little as $3.

Sourse: vox.com